A Senior Citizens Savings Scheme (SCSS) account is a retirement benefit account that is supported by the Indian government.

Indian senior citizens who invest a lump sum in the plan, either individually or jointly, can take advantage of the account's benefits.

Senior Citizens Savings Schemes can be availed by any individual above the age of 60 years.

SCSS Information

Tenure

5 years

Interest Rate

8.20% p.a.

Investment Amount

Maximum amount that can be deposited is Rs.30 lakh

Premature Withdrawal Allowed

The Senior Citizens Savings Scheme (SCSS) was launched with the main aim of providing senior citizens in India with a regular income after they attain the age of 60 years old. Some of the main benefits of the scheme are:

Tax benefits are provided.

Safe to invest in the scheme.

Process to Open an SCSS Account

An SCSS account can be opened at a bank or a post office.

Submit the application form along with the Know Your Customer (KYC) documents.

A cheque for the amount that is being deposited must be provided.

SCSS Eligibility

An individual who has attained the age of 60 years or above at the time of opening an SCSS account.

Individuals who have reached the age of 55 years old but are below the age of 60 years old and have retired on superannuation are eligible to open an SCSS account.

Individuals who have attained the age of 55 years old and have retired before the implementation of the SCSS rules are eligible under the scheme.

Non-Resident Indians (NRIs) are not eligible to open an SCSS account.

SCSS Interest Rate

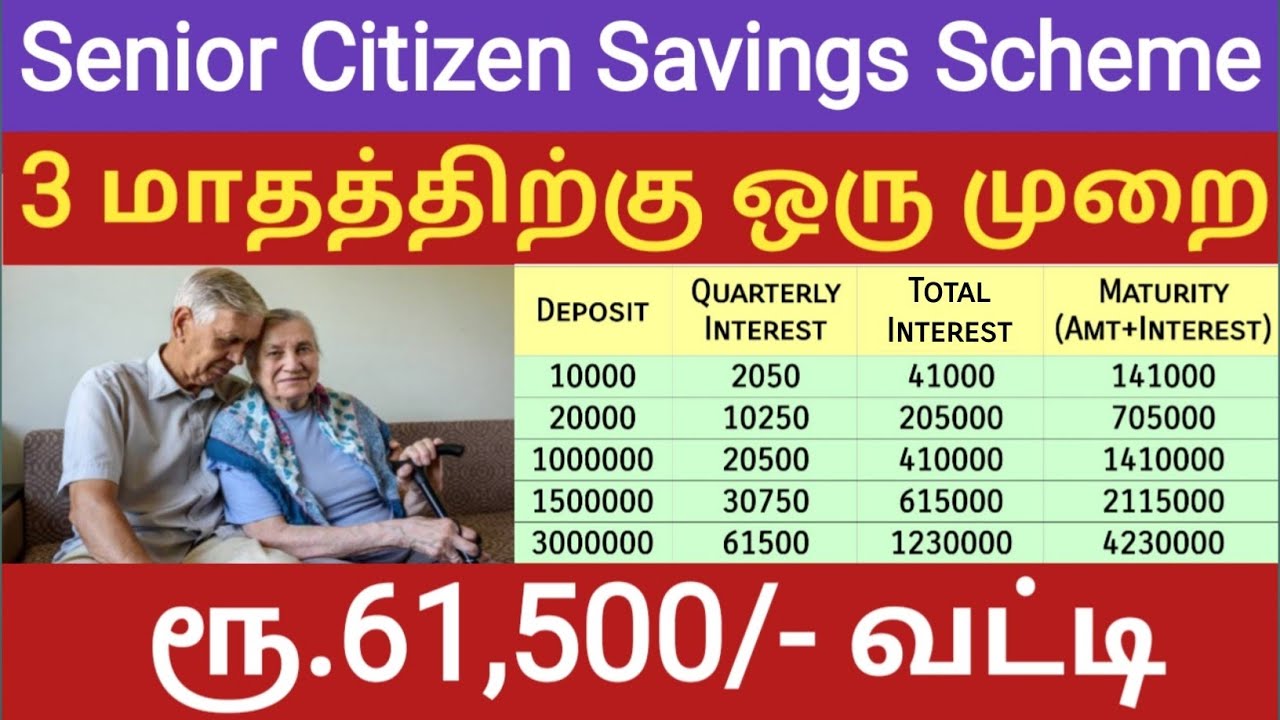

Currently, the SCSS interest rate is 8.20% p.a. The returns of the SCSS are high when compared to savings and Fixed Deposit (FD) accounts. Interest is payable on March 31, June 30, September 30, and December 31.

Quarterly interest is paid on the initial working day of April, July, October, and January.

How SCSS works?

Here are the details about how SCSS operates:

In a single instalment open an SCSS account by contributing of Rs.1000 to up to Rs.30 lakh

From the date of maturity, the account can be extended for another three years

The extension of the account can be done one year from the date of maturity

Benefits of SCSS

The following are the benefits of SCSS:

The SCSS account can be opened easily at any post office or authorised banks

The tenure of the SCSS account is five years which can be extended up to another three years

Income tax deduction can be availed for this scheme of up to Rs.1.5 lakh

Given below are the documents that individuals must submit in order to open an SCSS account:

Two passport-size photographs

Form A must be completely filled in and submitted.

Identity proof such as Passport or Permanent Account Number (PAN) Card must be submitted.

Individuals must submit proof of Aadhaar Card

A document confirming the individual's age must be submitted. Age proof document can be the Permanent Account Number (PAN ) Card, Voter ID, Birth, Aadhar

Maturity of the scheme:

The maturity period of the scheme is five years. However, individuals can extend the maturity duration for three years by submitting an application in the required format within one year of maturity of the account. However, the account can be closed without any charges after the expiry of the account.

Nominations available in this scheme

Number of accounts: Individuals are allowed to operate more than one account by themselves or open a joint account with their spouse.

Minimum and maximum amount: Only a single deposit is allowed to be made in the account. It can be in the multiples of Rs.1,000 and the maximum amount that can be deposited is Rs.30 lakh. Deposit amounts less than Rs.1 lakh can be paid by cash, while amounts more than Rs.1 lakh must be paid by cheque. In the case of cheque payments, the date the cheque realises will be the opening date of the account.

Transfer of an account: An SCSS account can be transferred from a bank to a post office and vice versa.

Premature withdrawal: After one year of opening the account, premature withdrawal is allowed. However, a 1.5% charge and a 1% charge of the total amount deposited will be charged in case of premature withdrawals after one year and two years, respectively

senior citizen saving scheme,

senior citizen saving scheme in tamil,

senior citizen saving scheme tamil,

senior citizen saving scheme in post office,

post office saving scheme in tamil,

senior citizen savings scheme,

post office saving scheme,

post office savings scheme,

senior citizen saving scheme post office in tamil,

post office saving schemes in tamil,

post office savings scheme in tamil,

SCSS,

scss scheme in tamil

#seniorcitizensavingsschemeintamil

#scssschemeintamil

#postofficeschemes

Chapters

00:01 - 00:42 - Introduction

00:43 - 02:10 - Definition and Eligibility

02:11 - 03:20 - How to open SCSS account

03:21 - 03:53 - Tenure and Int rate

03:54 - 04:34 - Int calc

04:35 - 05:16 - Pre-mature Closure

05:16 - 05:43 - Income tax benefits

05:44 - 06:51 - Example calculation

![[甄子丹 Donnie Yen 中國功夫|高清修復版] 洪熙官 1/30|愛國之士策劃反清復明|蔡曉儀、甄志強、張家輝、吳毅將|粵語中字|亞視經典劇集|Asia TVB Drama|亞視1994](https://i.ytimg.com/vi/1-8YYs4WXAA/mqdefault.jpg)