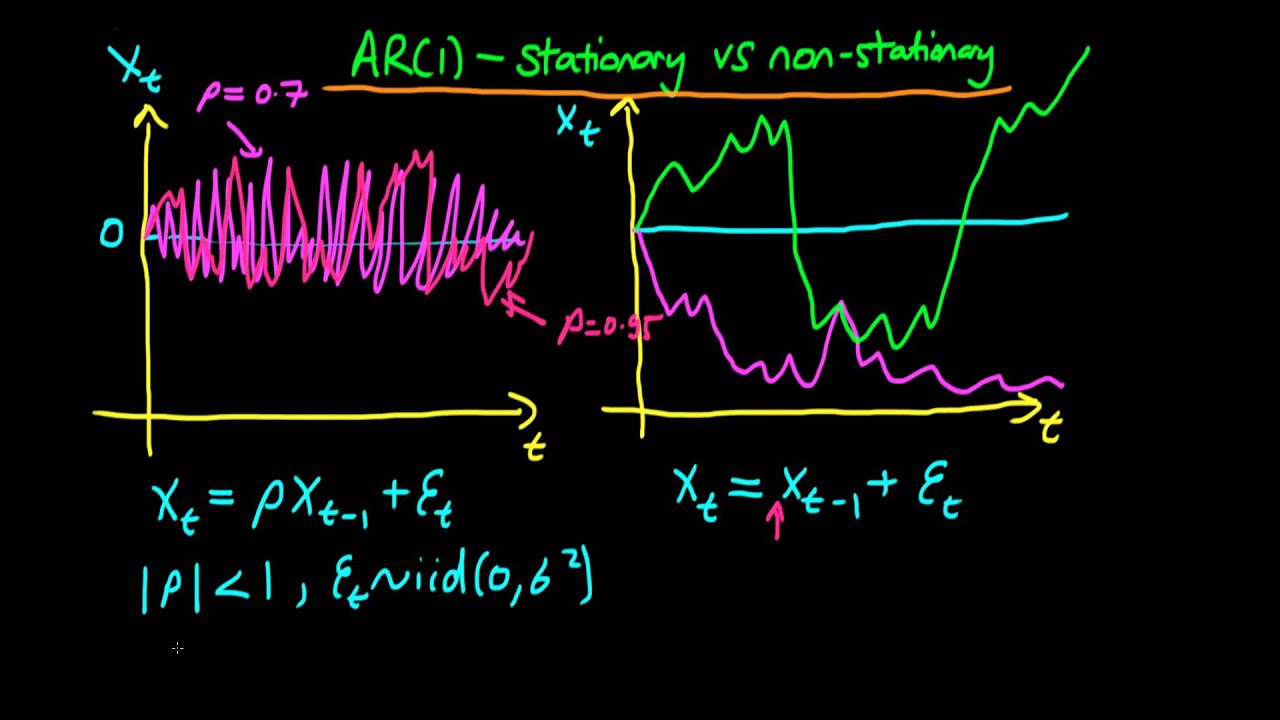

This video explains the qualitative difference between stationary and non-stationary AR(1) processes, and provides a simulation at the end in Matlab/Octave to demonstrate the difference.

clear; close all; clc;

n=10000; % Setting the number of time periods equal to 10000.

b=1;

rho=1; %This is the coefficient on the lagged part of x

x=zeros(n,1); % Initialise the vector x

x(1)=0;

for i = 2:n

x(i)=rho*x(i-1)+b*randn();

end

zoom=1.0;

FigHandle = figure('Position', [750, 300, 1049*zoom, 895*zoom]);

plot(x, 'LineWidth', 1.4)

ylabel('X(t)')

xlabel('t')

I also include the same in R (Courtesy of Jesse Maurais):

z = rnorm(1000)

gen = function(rho) {

x = numeric(length(z))

x[1] = z[1]

for (i in 2:length(z)) {

x[i] = rho*x[i-1] + z[i]

}

x

}

display = function(rho) {

x = gen(rho)

plot(x, main=as.character(rho))

lines(x)

}

for (it in 1:100) {

display(it/100)

Sys.sleep(0.5)

} Check out [ Ссылка ] for course materials, and information regarding updates on each of the courses. Quite excitingly (for me at least), I am about to publish a whole series of new videos on Bayesian statistics on youtube. See here for information: [ Ссылка ] Accompanying this series, there will be a book: [ Ссылка ]